The writer is an economist, anchor, and geopolitical analyst

and the President of All Pakistan Private Schools’ Federation

president@Pakistanprivateschools.com

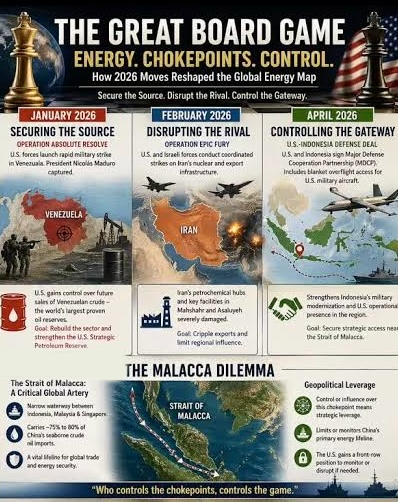

In an era of satellites, algorithms, and hypersonic missiles, global power still flows through narrow strips of water no wider than a few kilometres. Five critical maritime chokepoints—the Strait of Hormuz, Suez Canal, Strait of Malacca, Panama Canal, and emerging Arctic routes—collectively channel the overwhelming majority of world trade. Global trade is overwhelmingly maritime: roughly 80-90% by volume moves by sea. A handful of narrow passages concentrate this flow, creating extreme efficiency but also extreme fragility. These arteries do not merely facilitate commerce; they define it. Disruptions here ripple into inflation spikes, energy crises, and supply chain collapses that reshape economies continents away. Geography remains destiny, and those who control (or credibly threaten) these passages wield leverage disproportionate to their military or economic size.This is the Chokepoint Empire: not a formal alliance of empires, but a structural reality where control of canals and straits trumps traditional metrics of power. The “new great game” is less about conquering capitals than securing, bypassing, or weaponising these bottlenecks. Nations like Turkey, Egypt, Iran, and Singapore (along with their neighbours) punch far above their weight precisely because of their geographic positions. As climate change opens the Arctic and great-power competition intensifies, mastery of these passages will determine the winners of the 21st century. For three centuries, strategists measured power in capitals, coalitions, and carriers. The new century measures it in canals. Eighty per cent of global trade by volume, and over $9 trillion in goods annually, transits just five maritime chokepoints: Hormuz, Suez, Malacca, Panama, and the rapidly opening Arctic. Hormuz, Suez, Malacca, Panama, and the Arctic Control 80% of World Trade. You can sanction a country, but you cannot sanction a strait. You can bomb a factory, but if you lose a canal, you lose a continent’s supply chain. The great game has moved from embassies to estuaries. The Five Gates That Rule the World: Globalisation does not run on summits or silicon; it runs on straits. Five chokepoints — Hormuz, Suez, Malacca, Panama, and the emerging Arctic — form the circulatory system of the world economy, channeling 80% of trade by volume and over $9 trillion in goods each year. Hormuz bleeds 17 million barrels of oil and 30% of global LNG daily under the watch of Iran, Oman, and the UAE. Suez carries 12% of all trade and $1 trillion annually through Egypt’s hands. Malacca funnels 40% of global trade by volume — the lifeline for China, Japan, and Korea — past Singapore, Malaysia, and Indonesia. Panama moves 6% of world commerce and 40% of U.S. container traffic under Panama’s locks. And the Arctic’s Northern Sea Route, guarded by Russia and Norway, promises to siphon 20% of Asia–Europe trade from Suez by 2040. Block one, and you induce a heart attack in the global economy. That lesson turned lethal in February 2026 when Lloyd’s declared Hormuz a “Total War Risk Zone,” spiking premiums to 1.2% of hull value — $3.6 million per $300M VLCC, or $30.6 million daily extracted from Gulf producers. No missiles were fired; geography itself levied the tax. In the age of the chokepoint empire, sovereignty is no longer measured in capitals or carriers, but in who holds the keys to the gates through which the world must pass. The 20th century fought over ideology and air superiority. The 21st fights over flow. Strait of Hormuz: This 21-mile-wide (at its narrowest) passage between Iran and Oman serves as the sole maritime outlet for Persian Gulf oil and gas. Pre-2026 tensions, it carried about 20-21 million barrels per day of crude and petroleum products—roughly 20-25% of global maritime oil trade—plus significant LNG from Qatar and the UAE (about one-fifth of world LNG). Destinations are heavily Asian: China alone receives over a third of the flows. Events in 2026 demonstrated its lethality: following conflict, traffic plummeted to near-zero at points, spiking global oil prices and exposing dependencies. Even partial disruptions trigger insurance withdrawals, rerouting, and cascading shortages. Alternatives like pipelines are limited; Saudi and UAE bypass capacity exists, but cannot fully compensate, especially for Qatar’s LNG. Hormuz the Oil Jugular: Iran does not need to close Hormuz to weaponise it. Mining, missile threats, or even radar targeting from Bushehr raises insurance enough to reroute the supply. In the 2026 Iran War, no tanker was sunk. Yet Brent spiked to $142, and Jafurah FID was delayed because CDS spreads on Saudi Aramco widened 140 basis points. Hormuz is deterrence by geography — the threat is cheaper than the war. Suez Canal: Egypt’s man-made masterpiece links the Red Sea to the Mediterranean, shortening Europe-Asia voyages by thousands of miles. It handles 12-15% of global trade by value and up to 30% of container traffic. Annual goods value exceeds $1 trillion in normal times. Disruptions (e.g., the 2021 Ever Given grounding or Red Sea rerouting via Cape of Good Hope) add 10-14 days and massive fuel costs. Revenues for Egypt fluctuate but have peaked near $10 billion annually, making it a vital hard-currency earner. Suez the Weaponised Canal: Since 1869, Suez has been a toll road. Under the 2025 “Three Seas Initiative,” it became a weapon. Egypt, Pakistan, and Iran agreed: if any ISO member is struck, Egypt can deny Suez transit to aggressor-linked shipping under UN Article 51 self-defence. In February 2026, Cairo signalled ZIM Line would be barred if Israel struck Fordow. The strike was postponed. No shot fired. For the first time since 1956, Suez was not a neutral conduit but a sovereign lever. Strait of Malacca: The world’s busiest oil transit chokepoint, between Indonesia, Malaysia, Singapore, and Thailand. It carries ~22-25% of global maritime trade and ~29% of seaborne oil (23+ million barrels/day in recent data), plus LNG. Crucial for East Asia: ~80% of China’s oil imports and major flows to Japan and South Korea transit here. Over 100,000 vessels annually. Piracy, congestion, and potential toll disputes loom as risks. It is nearing capacity, prompting discussions of alternatives like land bridges. Malacca is the Pacific Bottleneck: China’s entire energy lifeline — 80% of its oil imports — transits Malacca. Singapore, sitting at its narrowest point, holds more coercive leverage over Beijing than Germany does. One reason ASEAN avoids taking sides: Indonesia, Malaysia, and Singapore know that whoever controls Malacca can throttle the factory of the world. The US Seventh Fleet patrols it; China builds pipelines to bypass it. The strait, not the summit, sets the terms. Panama Canal: Connecting the Atlantic and Pacific, it moves ~5-6% of global maritime trade but punches higher for the Americas—handling ~40% of U.S. container traffic on certain routes and significant bulk/agricultural goods. Droughts and water issues have constrained transits, highlighting climate vulnerabilities. Panama, the American Artery: 40% of U.S. container traffic uses Panama. Drought in 2023-2024 cut transits by 30% and added 14 days via Cape Horn. It cost U.S. retailers $2.8B. No invasion needed — climate and the canal authority did it. Panama’s neutrality is American prosperity. When the U.S. threatened to retake the canal in 2024, Panama City reminded Washington who controls the locks. Arctic Routes (Northern Sea Route/NSR along Russia, Northwest Passage via Canada): Not yet dominant but transformative. Melting ice shortens Asia-Europe routes by 30-50% versus Suez (NSR) or Panama (NWP). NSR already sees growing traffic for bulk, energy, and destination shipping; projections suggest 2-5% of global shipping by 2030-2050, potentially more. The Arctic is the Next Suez: Melting ice is opening the Northern Sea Route. Shanghai to Rotterdam via Suez: 22,000 km. Via Arctic: 13,000 km. Russia’s Rosatom now escorts LNG tankers with icebreakers. By 2040, 20% of Asia–Europe trade could shift north. That makes Russia, Norway, and Canada the new Egypts. The Bosphorus is no longer the only gate to the Black Sea; the Arctic is the gate to the 21st-century Silk Road. Together, these (plus related passages like Bab el-Mandeb and Turkish Straits) account for the bulk of critical flows. Analyses often cite ~80% of world trade funnelled through a small set of such vulnerabilities.

These chokepoints exist because geography and economics favour shortcuts. That’s why Trump’s return to the Security Council to pry open the Strait of Hormuz is not diplomacy — it is an admission that the era of unilateral guarantees is over. Having bypassed the UN with his ad hoc “Peace Board,” he now faces the institutional logic he tried to circumvent: if the Security Council is not ineffective, why was the Peace Board needed; if it is ineffective, why return to it now? The legal sleight of hand has boomeranged. China and Russia, both armed with vetoes, already torpedoed the Peace Board precisely because it lacked their veto, and they will not bless a resolution that repairs damage they believe Trump inflicted. Why would Moscow vote to reopen Hormuz when the closure has inflated its oil and gas leverage? Why would Beijing bail out a U.S.-led order while Washington arms Taiwan against China’s explicit will? The veto principle is binary — one “no” kills the text — and both powers can now ask the questions Trump avoided at the war’s onset: where was the Security Council before 16 bases burned, before the Iranian leadership that favoured talks was killed, before Hormuz became a 1.2% war-risk tax on the world economy? If Trump did not seek UN cover to start the conflict, why seek it to end the consequences? Russia and China will likely demand what the draft omits: recognition of Israeli aggression, guarantees against future war, and an acknowledgement that the strait’s closure is a symptom, not the disease. Without that, the resolution becomes a request for a free bailout of a crisis that the U.S. escalated. The Peace Board gambit exposed the weakness of hired shields; the Security Council gambit exposes the cost of using them. This time, China and Russia don’t just hold a veto. They hold the terms on which Hormuz reopens — and they can make Washington and Israel dance a triple dance to get it. The alternative—rounding Cape of Good Hope or Cape Horn—adds distance, time, fuel, and emissions. Just-in-time global supply chains amplify impacts: a week’s delay in containers or oil can halt factories, empty shelves, or spike fertiliser prices (Hormuz also carries significant volumes). Energy is the clearest vector. Oil and gas dominate, but containers, bulk commodities, and critical minerals flow too. Asia’s manufacturing heartlands depend on Middle East energy via Malacca and Hormuz. Europe relies on Suez. The Americas integrate via Panama. Arctic opening redraws this map, favouring Russia and potentially Canada while challenging traditional powers. Disruption costs are asymmetric. Producers lose export revenue; consumers face shortages and inflation; shippers pay premiums or reroute. In 2026 Hormuz events, insurance-driven halts showed how non-kinetic tools (threats + market reactions) can achieve blockade effects.

The Gatekeepers: Leverage of the Chokepoint Powers. Iran and Hormuz: Iran does not “own” the strait exclusively (Oman shares the south), but its coastline, missiles, drones, mines, and proxies give it credible denial power. Threats or limited actions can spike prices without full closure. This provides asymmetric leverage against superior navies—closing the strait hurts Iran too (its own exports), but the global pain buys diplomatic space or deters attacks. Recent conflicts underscored this “chokepoint as weapon.” Egypt and Suez: Egypt controls the canal outright. Tolls generate billions in revenue with minimal alternatives for many routes. While Egypt cannot easily “close” it without self-harm, rate hikes, maintenance policies, or security stances influence flows. It positions Egypt as indispensable, extracting economic and diplomatic value. Losses from past disruptions (e.g., billions in revenue) highlight stakes, but control remains a strategic asset. Turkey and the Turkish Straits (Bosphorus/Dardanelles): Via the 1936 Montreux Convention, Turkey regulates warship passage and holds significant discretion in wartime or perceived threats. This gives Ankara gatekeeper status over Black Sea-Mediterranean flows, including Russian energy/agricultural exports (~3% global oil via straits) and naval movements. Turkey balances NATO membership with independent leverage, as seen in Ukraine-related restrictions. It amplifies Turkey’s influence beyond its size.

The question is no longer who rules the world. It is who rules the gates — because whoever controls the strait, controls the state. The chokepoint empire has begun. Embracing Geographic Realism, indeed, the Chokepoint Empire reveals a timeless truth: technology compresses distance but does not eliminate geography. In a multipolar world of supply-chain weaponization, control of these passages confers veto power over segments of the global economy.

Singapore (and Malacca littoral states): Singapore thrives as a port and logistics hub precisely because of the strait. While transit passage is protected under UNCLOS (no unilateral tolls or closure), the littoral states (Singapore, Malaysia, Indonesia, Thailand) provide security, pilotage, and services. Coordinated patrols against piracy demonstrate cooperative leverage. Singapore emphasises freedom of navigation but benefits enormously from its position. Discussions of tolls (floated by others) reveal underlying power dynamics; Singapore pushes back to protect its model. These nations hold leverage because denial (or threat thereof) is cheaper than projection. Large powers must negotiate, escort, or reroute; gatekeepers can influence without matching fleets. The New Great Game is canals, not the capitals. Superpowers compete differently now. The U.S. maintains a naval presence near Hormuz and Malacca for freedom of navigation. China invests in port infrastructure (“String of Pearls” or Belt and Road) to secure routes, develops Arctic interests, and eyes alternatives. Russia promotes the NSR as a sovereign corridor. India diversifies imports and builds naval capacity. New infrastructure races include canal expansions, Arctic ports, and potential bypasses (e.g., Thai land bridge, pipelines). Climate change is the wildcard: Arctic opening could shift trade gravity northward, empowering Russia and Canada while marginalising traditional chokepoints—if ice, infrastructure, and governance challenges are solved. Hybrid threats rise: drones, mines, proxies, cyber, insurance manipulation, or “tolling” disputes. The 2026 Hormuz events blended kinetic and economic pressure. Non-state actors (pirates, Houthis) further complicate security. Resilience strategies include diversification (multiple suppliers and routes), stockpiles, nearshoring, and new technologies (larger ships, alternative fuels, land corridors). Yet substitutes are costly and slow to scale. Future Horizons: Arctic Ambitions and Beyond. The Arctic represents both opportunity and new chokepoints. The NSR could slash transit times, enabling year-round shipping with icebreakers and escorts. Russia invests heavily; China eyes a “Polar Silk Road.” Canada asserts sovereignty over the NWP. Environmental risks (oil spills, black carbon), indigenous rights, and governance (UNCLOS vs. coastal claims) will spark disputes. By mid-century, a navigable Central Arctic route could emerge. This redraws alliances: NATO vs. Russia-China axis in polar seas. Other emerging vulnerabilities include Bab el-Mandeb (Red Sea gateway to Suez), Danish Straits, and South China Sea tensions overlapping the Malacca approaches. From 1991 to 2023, the Gulf paid for U.S. protection in three currencies: oil priced in dollars, sovereign wealth in Treasuries, and arms with 40% markups. The hidden tax was war risk premiums. From 2019–2026, premiums went from 0.05% to 1.2%. That costs Gulf producers $11.1B per year — more than the price of a regional war. The U.S. model: “Buy our weapons, we might defend you.” The Chinese model: “Use our currency, we won’t defend you.” The guarantor model: “We station our sons in your deserts. If we die, we die together. Pakistan’s 4 air defence regiments in Saudi Arabia cost $1.2B, paid in oil credits. Equivalent U.S. THAAD coverage: $8B + 2,000 troops + Congressional approval. Pakistan deployed in 90 days. The U.S. took 18 months and attached conditions. This is why the hired shield died on 12 February 2026 when 16 U.S. bases burned. Conditional guarantees collapsed. The replacement is not a superpower, but a lattice of guarantor states tied to chokepoints: Pakistan at Hormuz, Turkey at the Bosphorus, Egypt at Suez, Indonesia at Malacca. The old measure of power was GDP and nukes. The new measure is: can you stop trade without firing a shot? Turkey controls the Bosphorus — Russia’s only warm-water exit and 3m barrels/day of Caspian oil. NATO needs Turkey more than Turkey needs NATO. When Ankara closed the straits to Russian warships in 2022, it altered the Black Sea war overnight. Egypt owns Suez. 12% of global trade pays Cairo tolls. When the Ever Given blocked it for six days in 2021, $60B in trade backed up. Egypt’s “Three Seas” doctrine now turns that vulnerability into a veto. No Suez, no war on Iran. Geography is Cairo’s nuclear weapon. Iran sits on Hormuz and shares it with Oman. It does not need a blue-water navy. A dozen AshCM batteries on Qeshm Island and drones from Bandar Abbas give Tehran escalation dominance over 20% of global oil. Sanctions cannot close a strait. Only Iran can. Singapore is a city-state with the GDP of Egypt, but it straddles Malacca. It hosts U.S. LCS, Indian naval logistics, and Chinese port investment. It trades in neutrality, and neutrality is now a superpower. When Singapore tightens port state control, supply chains shudder. None of these states has Germany’s industrial base or Canada’s landmass. But they can tax, deny, or delay the world economy. In the age of just-in-time logistics, a two-week delay is a recession. A one-week closure is a crisis. Chokepoints are sovereignty. Civilisation gets you in the room. Waterways keep you in the alliance. ISO coheres as Sunni-Shia-Arab-Persian-Turk not from theology, but because Hormuz and Suez bind them. NATO endures because the GIUK Gap demands it.

The 19th century belonged to empires that ruled the waves. The 20th belonged to superpowers that ruled the air. The 21st belongs to guarantor states that rule chokepoints. They do not need the largest GDP. They need the most relevant geography, the most credible risk-sharing, and the will to fight where they live. The old order was drawn along ideological blocs. The new order will be drawn along maritime corridors. The Persian Gulf–Mediterranean axis is the first. The Arctic and Malacca are next. You can sanction a country, but you cannot sanction a strait. And in the age of the guarantor state, whoever controls the livestream and the locks controls the order. The hired shield is gone. The age of the hired shield ended when capitals learned they cannot buy geography. Ideology does not transit the Strait of Hormuz. Aircraft carriers do not lower war-risk premiums at Lloyd’s. Treaties do not widen the locks at Panama. In the 21st century, sovereignty has migrated from constitutions to canals, from parliaments to passages, and from superpowers to canal lords. The new sovereigns do not sit in Washington, Beijing, or Brussels — they sit in Cairo, Tehran, Ankara, Singapore, and soon, Murmansk. They levy taxes no legislature voted on: 1.2% of hull value per Hormuz transit, 14 days added by a drought in Panama, a ZIM Line rerouted by a signal from Suez. They hold a veto that no Security Council can override, because you can sanction a country, but you cannot sanction a strait. Empires once ruled waves and air; now they rule flow. And flow is obedience. The chokepoint empire is not a metaphor. It is a ledger, written in basis points and barrels, and enforced by the simple fact that 80% of the world must ask permission from 5 narrow gates to eat, to fuel, to fight. Trump’s return to the Security Council to beg Hormuz open is the epitaph of unipolarity: when geography becomes destiny, even hegemons must negotiate with the map. The hired shield charged premiums for conditional protection. The canal lord charges tolls for unconditional passage. One was a promise. The other is physics. And in the age of the guarantor state, physics beats politics. Turkey, Egypt, Iran, and Singapore (plus neighbours) illustrate how “middle powers” or regional actors gain outsized roles. For the world, the imperative is clear: invest in resilience, diversify routes, strengthen international norms for unimpeded transit, and prepare for Arctic competition. For strategists, the lesson is ancient—secure the straits. Capitals rise and fall; canals and straits endure as arbiters of trade and power. The new great game is underway. Its board is water, its pieces are tankers and icebreakers, and its prizes are the narrow passages that still rule the world. Understanding this geography is the first step to navigating—or mastering—the future. In the grand theatre of civilisations, where armies clash and ideologies flare, true sovereignty has never resided in fleeting parliaments or gilded thrones but in the silent, unyielding grip of geography itself. The Chokepoint Empire endures not through conquest, but through mastery of the narrow veins that pulse with the world’s lifeblood—those razor-thin canals and straits where Canal Lords, the unseen sovereigns of our age, dictate the rhythm of global commerce, starve rivals with the turn of a valve, and crown empires with the stroke of a map. As satellites swarm the skies and digital phantoms promise borderless freedom, we are reminded with crystalline force that the ultimate power remains terrestrial, ancient, and merciless: control the chokepoints, and you command the future. In this truth lies both warning and revelation—whoever masters the map’s fatal bottlenecks will not merely rule the world; they will redefine what “world” even means. The question is no longer who rules the world. It is who rules the gates — because whoever controls the strait, controls the state. The chokepoint empire has begun. Embracing Geographic Realism, indeed, the Chokepoint Empire reveals a timeless truth: technology compresses distance but does not eliminate geography. In a multipolar world of supply-chain weaponisation, control of these passages confers veto power over segments of the global economy.