The writer is an economist, anchor, geopolitical analyst and the President of All Pakistan Private Schools’ Federation

president@pakistanprivateschools.com

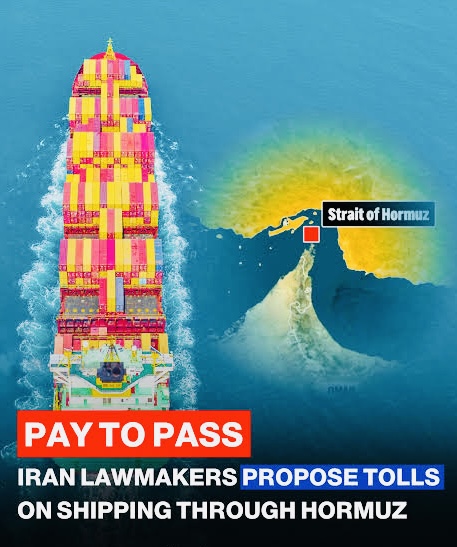

The 48-hour ultimatum collapsed under its own asymmetry: when Trump threatened Iran’s power plants, Tehran replied in the language of reciprocal blackout—strike ours, and the Gulf’s grids and desalination plants, including Israel’s, go dark too—and Washington blinked. Pakistan, flanked by Turkey and Egypt, stepped into the breach, and the strikes were paused for five days while an Iranian official distilled Tehran’s real terms: a simultaneous ceasefire across Iran, Lebanon and Iraq; no negotiation on the missile program (defensive, non-negotiable, and set to intensify under any truce); enrichment to continue, independently or with China and Russia; and compensation for U.S.–Israeli damage. Iran’s public line—“you hit our hospitals, schools and emergency centers; we didn’t do the same, but touch our power plants and we will”—framed the standoff as a war of survival that Washington, fearing “huge” retaliation across Israel and the Gulf, chose not to test. On the other side, In a dramatic escalation amid ongoing regional tensions, Iranian lawmakers have floated a sweeping proposal to impose tolls and “security taxes” on vessels transiting the Strait of Hormuz. Iranian Foreign Minister’s while addressing to the International Community said “Let me put it plainly: Egypt bills $200,000–$700,000 for a Suez transit—and more than $1 million for the biggest container ships and tankers. Panama takes $100,000–$450,000, up to half a million for a New Panamax. Turkey levies its own dues on the Bosphorus; Canada and the United States both charge for the St. Lawrence Seaway. Iran, by contrast, has kept the Strait of Hormuz free for decades—no toll, no invoice—while absorbing sanctions, isolation, and the “rogue” label. So forgive the dissonance: everyone monetizes their chokepoint, yet when Tehran talks about a security fee to keep passage safe, it alone is cast as the villain.” A Tehran parliamentarian, Somayeh Rafiei, stated on March 19, 2026, that parliament is advancing legislation requiring countries using the strait for shipping, energy transit, and food supplies to pay fees to Iran as compensation for maintaining security. “The security of the strait will be established with strength, authority and grandeur by the Islamic Republic of Iran, and countries must pay a tax in return,” she declared. Sensational headlines on media have amplified this into claims of an immediate, blanket “huge decision” with no exemptions and a full blockade for non-payers—“starting today.” In reality, the measure remains a parliamentary bill under review, not yet enacted law. However, selective implementation has already begun: Iranian officials confirmed in late March 2026 that at least one private oil tanker operator paid approximately $2 million for safe passage, with negotiations underway for others. Iran at the same time also played a Petro-Yuan Gambit by a strategic challenge to the Petrodollar and the emerging multipolar world order. The global financial architecture has rested for decades on the petrodollar system — the convention established in the 1970s whereby major oil-exporting nations, led by Saudi Arabia, price and settle their crude sales predominantly in U.S. dollars. This arrangement cemented the dollar’s status as the world’s primary reserve currency, granting the United States unparalleled economic leverage through seigniorage, sanctions power, and control over global liquidity. In early 2026, amid escalating regional tensions, Iran has floated a provocative counter-strategy: conditioning safe passage for oil tankers through the Strait of Hormuz — the chokepoint carrying roughly 20% of global seaborne oil trade — on the use of the Chinese yuan for transactions. This move, widely reported in mid-March 2026 via CNN and other outlets citing Iranian security sources, represents far more than a bilateral currency swap. It is an asymmetric economic weapon aimed at accelerating de-dollarization, deepening the Iran-China strategic partnership, and reshaping alliances across Eurasia and the Global South. Reports indicate Tehran is negotiating with eight countries (primarily outside the Middle East) to grant safe passage to yuan-denominated oil shipments. While the query referenced “twenty countries,” available public reporting consistently points to eight active discussions, with broader interest from oil buyers seeking alternatives amid sanctions and conflict risks. In this situation, Trump still performs “very strong talks” for the markets; Tehran reads the mixed U.S. signals as theater for mediators. And in the background, Sindoor quietly reset another ledger: the world’s old assumption of Indian conventional superiority has been dented, Pakistan’s defense prestige—and with it, Riyadh’s calculus—has risen, and the region learns again that ultimatums age badly when the other side is willing to turn the lights out everywhere. The market told the truth before the press releases did: a hint of “constructive talks” and a five-day pause on striking Iran’s power plants puffed stocks by $2 trillion; Tehran’s refusal to play along yanked $3 trillion back out, a swing that reads like a vote of confidence in Iranian signaling over Trump’s. The deterrent that moved the needle wasn’t rhetoric but reciprocal blackout—Iran warned that hitting its grid would mean the lights and desalination plants go dark across Saudi Arabia, the UAE, Qatar, Bahrain and Iraq, with the Houthis ready to choke the Red Sea and seal Hormuz. Two Israeli cities were hit, Dimona was struck through five layers of defenses (Patriot, Arrow, Iron Dome—all suddenly mortal), and an alleged “false-flag” claim about a British base muddied the narrative just as critical voices rose in Washington. The strategic sky darkened further with rumors of a Russian “nuclear shield” over Iran—Colonel Douglas Macgregor’s claim that Putin warned Netanyahu of a Russian nuclear response to any nuclear use in the region—while Moscow’s ambiguity deepened Israeli unease and fed talk that Israel’s nuclear deterrent has lost its aura. The energy crisis, the strait’s closure risk, and relentless salvos have lifted this from a regional duel to a three-cornered nuclear balance. Regime change looks like a mirage, Gulf capitals lean on Trump to de-escalate, and a president who tried to price a war in 48-hour increments is discovering he has no clean exit. This marks a shift from rhetoric to ad-hoc enforcement in the midst of the broader U.S.-Israel-Iran conflict. This development carries profound implications for global energy security, shipping costs, and geopolitics. The Strait of Hormuz handles roughly 20 million barrels per day (mb/d) of crude oil and petroleum products—equivalent to about 20% of global oil consumption and 25% of seaborne oil trade—plus around 20% of global LNG shipments. Nearly 100 cargo vessels pass daily, with 80-89% of flows destined for Asia. The Strait of Hormuz in context that the narrow waterway (as little as 21 miles wide at its narrowest) lies between Iran and Oman, with shipping lanes hugging territorial waters. Unlike artificial canals, it is a natural international strait governed by the United Nations Convention on the Law of the Sea (UNCLOS), to which Iran is a signatory. UNCLOS guarantees “transit passage” rights—continuous and expeditious navigation without interference. Imposing unilateral tolls or selective permissions raises serious legal questions, as experts note it could violate these freedoms and invite international challenges or naval pushback. The proposal emerges against a backdrop of disrupted flows from attacks on energy infrastructure and a de facto partial closure, already driving Brent crude above $100–106 per barrel in March 2026. Markets are pricing in prolonged risks, with executives planning for $175 oil scenarios and supply shortages in Asia.

Geopolitically, this is Iran leveraging its de facto control in wartime, mirroring historical threats but now monetizing rather than solely blockading. Gulf neighbors (Saudi Arabia, UAE) have warned of military responses, while the U.S. maintains freedom-of-navigation patrols. Success depends on enforcement feasibility against international naval presence. By comparison with other major tariff routes to assess the potential disruption, it is essential to compare Iran’s move with established chokepoints that already levy transparent, non-discriminatory tolls. Suez and Panama serve as benchmarks: sovereign-managed waterways with predictable pricing that generate stable revenue without halting trade. In contrast, Hormuz’s proposed system appears selective, security-framed, and far costlier per vessel. By 2025–26 the Strait of Hormuz has become less a chokepoint than a tollbooth in a war zone: an Iranian parliamentary bill hands Tehran the manager’s keys, and the “fee” is not a published tariff but a security/transit tax levied case by case—one large crude tanker has already been billed about $2 million, with only hand-picked vessels granted “permission” to pass. The leverage is staggering—roughly 20 million barrels of oil a day plus a fifth of the world’s LNG squeeze through a 21-mile seam—but the revenue model is untested, unstable, and welded to escalation risk, as Gulf states and a U.S.-led coalition weigh military answers. Rerouting around the Cape of Good Hope adds two to four weeks and a fuel penalty that punishes the global economy more than it disciplines Tehran, turning a narrow waterway into a geopolitical paywall where the price isn’t set by markets but by missiles. Suez Canal in Egypt where Suez Canal Authority (sovereign but international treaty legacy). Where tiered rates based on Suez Canal Net Tonnage (SCNT) in SDR per ton; separate categories for crude oil tankers, petroleum products, LNG/LPG carriers, etc. Ballast discounts apply; additional surcharges possible. Typical cost: $300,000–$700,000+ for Suezmax/VLCC tankers or ultra-large container ships; can exceed $1 million with extras. Whereas, at Panama Canal in Panama, Panama Canal Authority (post-1999 treaty), where Dual structure—fixed fee by vessel category/locks ($60,000–$300,000 for most commercial ships) + capacity-based rates. The volume is lower oil share but critical for U.S.–Asia trade. Other Notable Chokepoints: Bab el-Mandeb Strait: No formal tolls; gateway to Suez but plagued by Houthi attacks (no state taxation); Strait of Malacca: Fully international; zero tolls, though piracy/escort costs occasional; Turkish Straits (Bosphorus/Dardanelles): Turkey imposes some navigation/service fees but not blanket transit taxes. Established routes like Suez and Panama operate as commercial infrastructure with clear rules, benefiting the host nation (Egypt derives 5–10% of GDP indirectly from Suez revenues) while upholding freedom of navigation. Tolls are tonnage- or capacity-based, applied uniformly, and far lower per transit than Iran’s reported $2 million flat fee. A Suezmax tanker might pay under $500,000 at Suez versus a potential multimillion-dollar demand at Hormuz—potentially 4–8× higher. Iran’s framing as a “security tax” for permitted vessels introduces discrimination: exemptions or higher rates for adversaries could fragment trade, favoring allies (e.g., China) while punishing others. This contrasts sharply with the neutral, treaty-backed models of Suez (1869 convention legacy) and Panama (1977 treaties). Legally, UNCLOS transit passage does not permit arbitrary fees or suspensions; any enforcement risks confrontation, as seen in joint statements from over 20 nations condemning interference. Economically, the proposal—layered on existing war disruptions—amplifies risks. Rerouting via the Cape of Good Hope adds 10,000+ nautical miles, spiking bunker fuel, insurance (war-risk premiums already surging), and delivery times. Global inflation, aviation, and Asian manufacturing could face sustained pressure if flows drop or costs rise. Markets have already repriced oil higher; a formalized Hormuz toll system could embed a permanent premium, unlike the recoverable shocks at Suez (post-2023–2025 Red Sea issues) or Panama (drought 2023–2024). If the bill passes and scales beyond selective $2 million charges, the Strait of Hormuz would transform from a free international chokepoint into a high-cost, permission-based toll route—fundamentally altering 20–25% of global energy flows in ways Suez and Panama never have. Short-term, it exacerbates current price spikes and supply uncertainty. Long-term, it could accelerate diversification but at immense transitional cost. The “huge decision” remains aspirational for now, but the precedent of even partial fees signals a new era of weaponized chokepoints. Global stakeholders—shippers, importers, and navies—must prepare for higher volatility, as one strait’s taxation ripples across the entire maritime tariff ecosystem. In an interconnected world, Iran’s move underscores a harsh truth: the most vital routes are those most vulnerable to unilateral control. At the same time, Iran’s deepening economic and infrastructural alignment with China — including long-standing elements of their 2021 Comprehensive Strategic Partnership — has fueled speculation about port dynamics in the region. Contrary to claims of an outright “handover” of port to Beijing, current realities show India retaining operational control under a 10-year agreement signed in 2024–2025, albeit with funding uncertainties due to U.S. sanctions pressures. However, any erosion of Indian involvement could open space for greater Chinese participation, creating synergies with Pakistan’s Gwadar port (a flagship of China’s Belt and Road Initiative). This linkage would amplify Pakistan’s geopolitical weight and solidify a China-centric corridor across South and West Asia. The petrodollar system emerged after the 1973 oil crisis when the U.S. struck deals with Saudi Arabia and other Gulf producers to recycle petrodollars into U.S. Treasuries and arms purchases. This recycled oil revenues into American financial markets, suppressed U.S. borrowing costs, and enabled the dollar’s dominance even after the end of the gold standard in 1971. Today, approximately 80% of global oil trade remains dollar-denominated, reinforcing U.S. extraterritorial sanctions (e.g., against Iran, Russia, and Venezuela). Iran has long chafed under this regime. Successive U.S. sanctions since 1979, intensified after the 2018 withdrawal from the JCPOA nuclear deal, forced Tehran into shadow fleets, barter arrangements, and non-dollar trade. China — already Iran’s largest oil buyer — has purchased Iranian crude via yuan-settled deals through intermediary networks and the Shanghai International Energy Exchange’s petroyuan futures launched in 2018. Russia similarly shifted to ruble/yuan pricing post-2022. Iran’s latest Hormuz proposal escalates this from defensive circumvention to offensive leverage: access to the world’s most vital energy artery now carries a currency condition. Under the reported framework, Iran would permit a limited number of tankers through the Strait of Hormuz — closed or heavily disrupted amid 2026 hostilities — only if the underlying oil cargo is traded and settled in yuan. China already moves Iranian oil freely under this model; formalizing it for others could create a parallel yuan-denominated oil corridor. This is as a bifurcated global oil market: yuan barrels flowing efficiently for willing buyers, while dollar-dependent shipments face rerouting, higher insurance, or exclusion. Yuan transactions evade SWIFT and U.S. secondary sanctions more effectively, using China’s Cross-Border Interbank Payment System (CIPS). Yuan internationalization boosts demand for renminbi reserves among oil importers, supporting Beijing’s long-term goal of challenging dollar hegemony without full convertibility. Which signals to OPEC+, BRICS nations (Iran joined in 2024), and sanctioned producers that alternative pricing is viable. China has responded cautiously; analysts in Beijing cite operational risks, insurance complexities, and the yuan’s limited global liquidity. Yet the architecture already exists: shadow fleets protected by Iran’s IRGC have delivered 11–16 million barrels daily to China since late February 2026. This shift carries profound ripple effects: If even 10–20% of Hormuz traffic migrates to yuan pricing, it accelerates a trend already visible in BRICS de-dollarization talks, Asian Clearing Union initiatives, and Gulf states exploring non-dollar oil sales. Historical parallels — Iraq’s 2000 euro switch or Libya’s gold dinar proposals — ended in regime change; Iran’s move tests whether the U.S. can respond similarly in a multipolar era. Economists like Yanis Varoufakis have noted that requiring yuan reserves for Hormuz access quietly shifts global reserve preferences away from dollars; The 2021 25-year $400 billion Comprehensive Strategic Partnership, though delivery has lagged (actual Chinese investment in Iran remains modest compared to Gulf neighbors), provides the backbone. Iran gains economic lifelines and diplomatic cover; China secures discounted energy, a foothold in the Persian Gulf, and BRI connectivity. This partnership counters U.S.-Israel pressure and integrates Iran into Eurasian supply chains; the impact on Global Energy Security and Markets: Oil prices spiked above $100/barrel in early 2026 amid disruptions. A yuan-conditioned Hormuz could add premiums for dollar users, inflate costs for Europe, India, and Japan, and spur hedging via Shanghai futures. Emerging markets may stockpile yuan, pressuring dollar demand and U.S. interest rates; Regional realignments in the West and South Asia. Feasibility hurdles abound: the yuan’s partial convertibility, limited acceptance outside China-aligned states, insurance and logistics complexities, and potential U.S. naval enforcement. Chinese observers urge caution over security risks in a volatile strait. Iran’s economy remains fragile; over-reliance on China risks new dependencies. Global oil majors and importers may resist bifurcation.

Whether this gambit succeeds depends on adoption by the eight, and potentially more, negotiating nations, China’s willingness to backstop the system, and Washington’s response. What is clear is that Iran, long a sanctions outlier, has weaponized its geography to accelerate a trend decades in the making — one that could redefine alliances, trade routes, and power balances for generations.

Iran’s Petro-yuan initiative and sweeping proposal to impose tolls and “security taxes” on vessels transiting the Strait of Hormuz is a “Watershed Moment” in the decline of “Unipolar Finance” for leverage and amplified by China’s infrastructural shadow (including potential Chabahar synergies with Gwadar), marks a deliberate step toward upending the global order. It does not instantly dethrone the dollar — which retains deep liquidity, trust, and network effects — but normalizes alternatives at a critical juncture of geopolitical flux. Pakistan emerges as a key beneficiary through Gwadar’s enhanced centrality, while India faces strategic recalibration. The world order is transitioning from dollar-centric unipolarity to a contested, multi-currency multipolarity, with energy flows as the battleground. Whether this gambit succeeds depends on adoption by the eight (and potentially more) negotiating nations, China’s willingness to backstop the system, and Washington’s response. What is clear is that Iran, long a sanctions outlier, has weaponized its geography to accelerate a trend decades in the making — one that could redefine alliances, trade routes, and power balances for generations. The petrodollar era is not ending overnight, but in the Strait of Hormuz and the ports of Chabahar and Gwadar, its foundations are visibly cracking.

The writer is an economist, anchor, geopolitical analyst and the President of All Pakistan Private Schools’ Federation

president@pakistanprivateschools.com